By: DSIRE Insight Team

The year 2019 was an exceptionally busy one for state energy policy, and the DSIRE Insight team at the North Carolina Clean Energy Technology Center is working to help you follow all of the action. The team recently released the Q4 2019 and 2019 Annual Review editions of the 50 States of Solar, Grid Modernization, and Electric Vehicles reports. These reports track all of the proposed state bills and regulatory proceedings in the policy areas of distributed solar, grid modernization, and electric vehicles, allowing readers to follow the details of state policy changes while also getting a sense of big picture policy trends across the United States.

Record Numbers of Actions

The three reports found that a record number of actions [1] were under consideration over the entirety of 2019. While the increase in number of actions was very modest for distributed solar (265 actions in 2019 vs. 264 in 2018), both grid modernization (612 actions in 2019 vs. 460 in 2018) and electric vehicles (601 actions in 2019 vs. 424 in 2018) saw huge jumps in activity this year. The number of policy actions in grid modernization and electric vehicles has more than doubled since 2017.

50 States of Solar

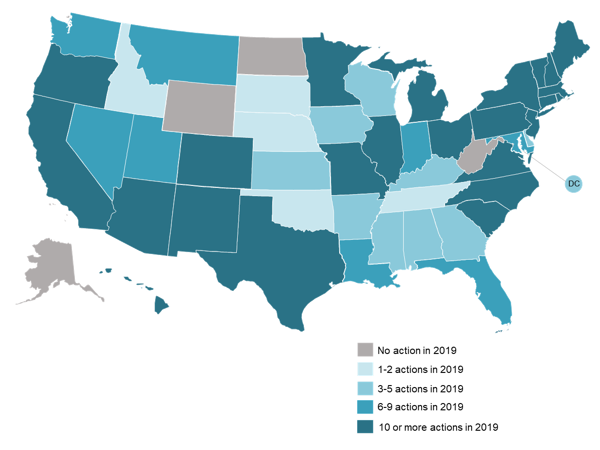

While the total number of policy actions for distributed solar did not change much in 2019, the types of actions under consideration shifted considerably. Fixed and solar-specific charge proposals declined in 2019; utilities proposed fewer and smaller fixed charge increases during 2019 than in previous years, and no utilities proposed mandatory residential demand charges. Some utilities did propose charges based on solar system capacity, but only one of these was approved. Replacing the activity on fixed charges and additional fees were actions on community solar program rules (many of them seeking to increase low-income participation), actions on incorporation of solar-plus-storage systems into interconnection rules and crediting systems, and actions on third-party ownership options. and

2019 Action on Distributed Solar Policy & Rate Design

Action on net metering and related compensation systems for distributed solar continued in 2019. Several states initiated the move to net metering successor tariffs, while others initiated value of solar studies to inform the development of successor tariffs in the future. Some states elected to retain traditional net metering after consideration of successor tariffs, and one state returned to traditional net metering from a successor tariff adopted in a previous year. In addition to these actions on crediting rules, 2019 also saw many actions refining net metering program rules to establish different customer classes, increasing system size limits, and adopting rules for solar-plus-storage systems.

50 States of Grid Modernization

Grid modernization refers to actions seeking to make the grid more resilient, responsive, and interactive, among other goals, and is used to describe a wide range of topics including both deployment of new technology and adoption of new policies, utility business practices, and rate designs. All of these topics interrelate, and utility commissions have increasingly recognized and acted on this interrelation. State regulators denied several utility technology deployment proposals in 2019 because the utilities did not demonstrate how the technology deployments would be coupled with rate design changes in order to maximize customer benefits.

2019 Action on Grid Modernization, Energy Storage, & Utility Reform

Although proposals for new technology deployments and technology incentive programs increased in 2019, consideration of more fundamental policy changes also emerged as action categories. Several states considered or are now considering major utility business model reforms, such as introducing retail competition and joining regional wholesale markets. Many states are also considering new utility performance incentive mechanisms and advanced rate design pilots.

Energy storage remains a key part of the grid modernization policy environment. Proposals for energy storage deployment were again the most common single type of action, and many other policy actions, such as changes to integrated resource planning and distribution system planning, updates to interconnection standards, and additions to energy efficiency and demand-side management plans, are taking place in order to incorporate energy storage into the electric system.

50 States of Electric Vehicles

Electric vehicle policy activity has expanded dramatically since our tracking began in 2017. While the raw number of actions under consideration has grown, another notable indicator of activity is the geographic spread of electric vehicle policy action. Forty-nine states and DC considered electric vehicle policy, regulation, studies, and deployment in 2019, with only West Virginia not addressing these issues. This makes electric vehicles the most geographically widespread category out of the three reports, as both distributed solar and grid modernization saw action in 46 states and DC.

2019 Action on Electric Vehicles & Charging Infrastructure

States are grappling with several major policy questions as electric vehicle use and infrastructure development expands. One question is whether to regulate providers of electric vehicle charging stations as public utilities. In 2019, states that considered this question universally decided that the answer is “no.” All states that reached a conclusion on the public utility regulation question during 2019 decided not to regulate charging stations as public utilities, opening the market to third-party providers. However, states have taken different approaches on the related question of whether utilities are allowed to own charging infrastructure.

Another major policy question is whether (and how) to charge electric vehicle owners an additional fee in order to make up for the reduction in gasoline tax revenue associated with electric vehicle use. Ten states elected to increase electric vehicle registration fees during 2019, with the additional fees ranging from $50 to $225. Some states have considered more complicated methods for recouping road infrastructure costs from drivers, such as mileage or vehicle weight-based charges, but all of the new fees going into effect have been simple fixed annual fees, although often with differentiated fees for all-electric and hybrid vehicles.

States and utilities are also considering a variety of policies and programs to spur electric vehicle use. Some states are requiring utilities to develop comprehensive transportation electrification plans, providing incentives for electric vehicle or charging infrastructure purchases, or adopting procurement targets for state government vehicle fleets. Utilities are also taking independent steps to increase electrification, such as proposing bus electrification programs, subscription pricing pilots, and rate design innovations to promote DC fast charger development.

Looking Ahead

The year 2020 figures to be another busy one for policy actions in distributed solar, grid modernization, and electric vehicles. It will be interesting to see what existing trends continue and new trends emerge. For access to all of these reports as well as detailed biweekly policy tracking, please consider subscribing to DSIRE Insight.

[1] An action is defined as a relevant (1) bill that has been introduced or (2) a regulatory docket, investor-owned utility rate case, or rulemaking proceeding. For the 50 States of Solar, only proposed legislation that has passed at least one chamber is included.

* * *

View the executive summaries or purchase full copies of the latest 50 States reports here. For more information, email us at afproudl@ncsu.edu.